Table of Contents

- Introduction

- What Is Real Estate Tokenization?

- The Mechanics of Real Estate Tokenization

- Key Benefits of Tokenizing Real Estate

- Challenges and Risks

- Regulatory Landscape by Jurisdiction

- KYC/AML Compliance

- Pioneering Platforms and Live Projects

- Market Data and Growth Projections

- The Road Ahead: Trends and Predictions

- Conclusion

- Sources and References

1. Introduction

The global real estate market is the world’s largest asset class, valued at over $300 trillion, yet it remains notoriously illiquid, opaque, and inaccessible to the average investor. A traditional property transaction can take months, involves layers of intermediaries—brokers, lawyers, notaries, title companies—and demands substantial upfront capital. Once purchased, the owner’s wealth is locked into the physical asset until an outright sale, which may take years.

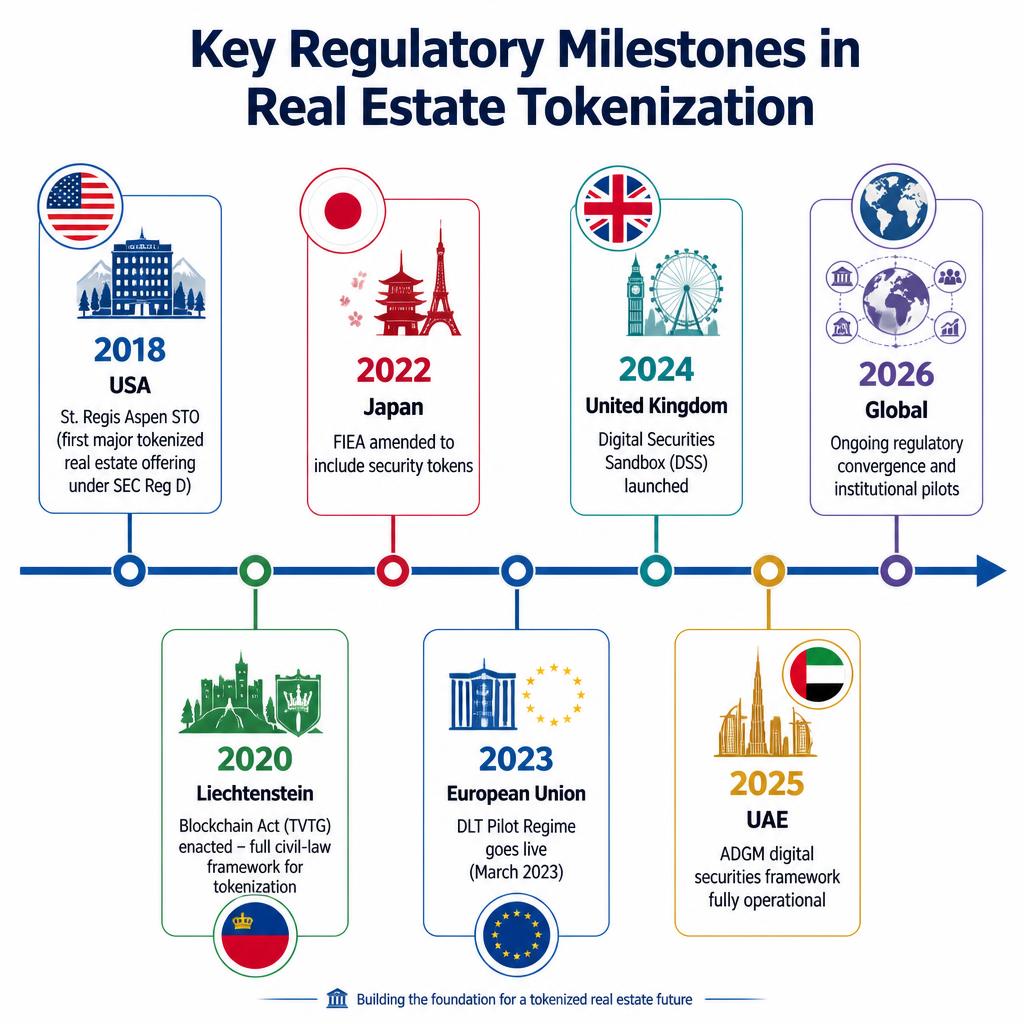

Real estate tokenization is changing this paradigm. By representing ownership rights as digital tokens on a blockchain, property becomes as tradable as a stock, divisible into affordable fractions, and accessible to a global pool of investors. The concept, once dismissed as a crypto-utopian experiment, has gained real-world traction. In 2018, the St. Regis Aspen Resort raised $18 million through a Security Token Offering (STO), marking the first major tokenization of a trophy asset. Since then, thousands of properties—from single-family rentals in Detroit to luxury apartments in Dubai—have been tokenized, with platforms like RealT and Lofty AI surpassing a combined $180 million in tokenized real estate by early 2025.

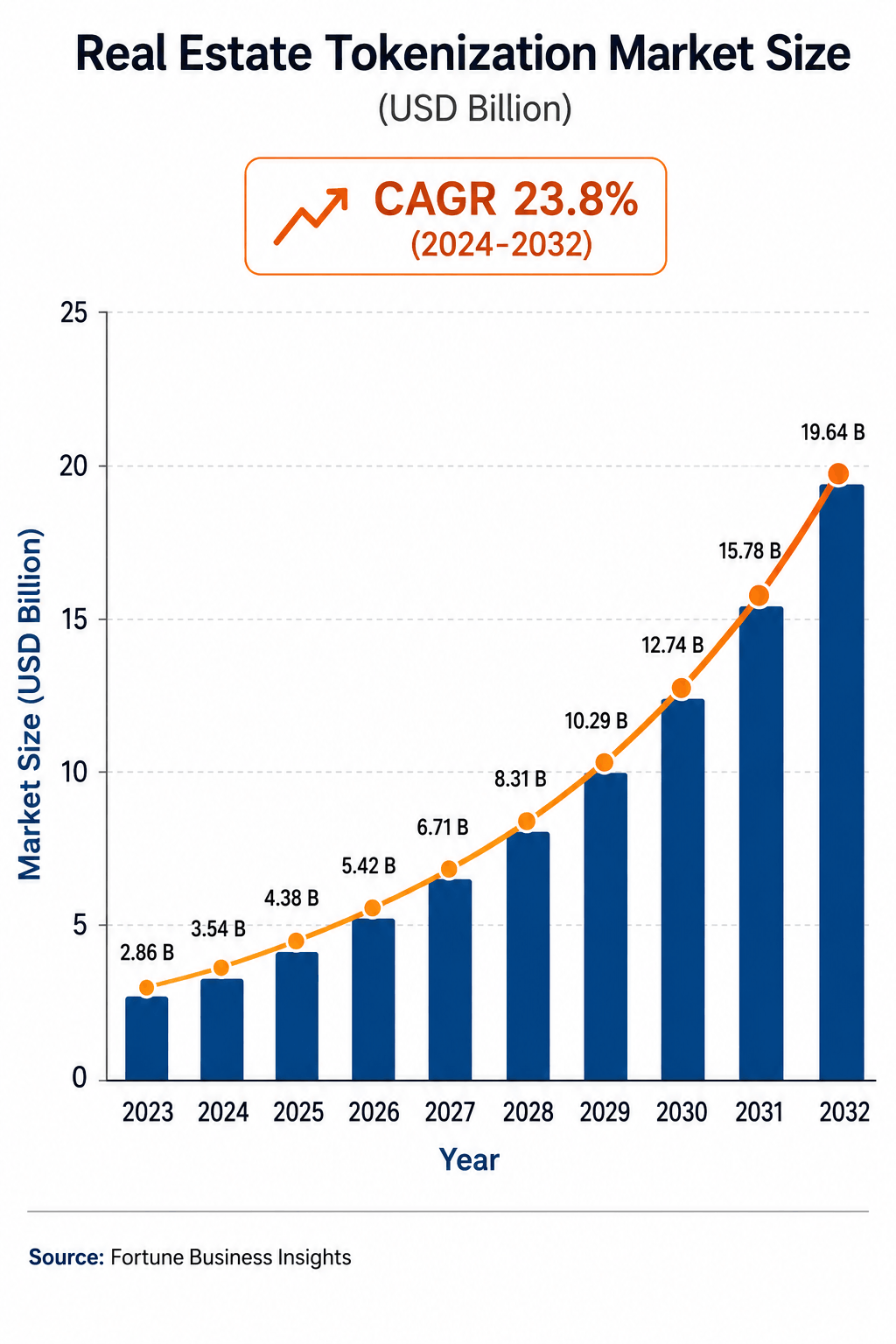

According to Fortune Business Insights, the global real estate tokenization market was worth $2.86 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 23.8%, reaching $19.64 billion by 2032. This growth is driven by maturing blockchain infrastructure, clarifying regulatory frameworks, and a global search for yield in a low-liquidity environment.

This pillar article provides a comprehensive, fact-based, and up‑to‑date guide to real estate tokenization as of mid‑2026. It covers the underlying technology, the legal and regulatory patchwork across ten key jurisdictions, the indispensable role of Know‑Your‑Customer (KYC) and Anti‑Money Laundering (AML) compliance, the most significant live projects, and the trends shaping the future of tokenized property. All information is drawn from official sources, platform disclosures, and regulatory publications, ensuring accuracy and relevance.

2. What Is Real Estate Tokenization?

Real estate tokenization is the process of issuing digital tokens on a blockchain that represent a fractional ownership interest in a specific property or a portfolio of properties. These tokens are security tokens, meaning they are subject to securities laws and confer economic rights such as a share of rental income, profit distributions, and sometimes voting rights. Unlike cryptocurrencies, which are typically unbacked digital assets, tokenized real estate tokens are asset‑backed and derive their value from the underlying physical property.

The concept marries two worlds: the centuries‑old legal framework of real estate ownership and the 21st‑century programmability of distributed ledger technology (DLT). By tokenizing a property, the issuer can break it into hundreds or thousands of digital shares, each represented by a token that can be bought, sold, or traded on compliant secondary markets. This turns a traditionally illiquid asset into a tradeable instrument, opening up real estate investing to retail participants who can now purchase a fraction of a property for as little as $50.

The term “tokenization” can refer to the entire lifecycle: selecting the property, setting up a legal structure (typically a Special Purpose Vehicle), minting the tokens, conducting the primary offering, and enabling secondary trading. Throughout this lifecycle, compliance with securities laws, KYC/AML regulations, and property‑specific rules remains paramount.

3. The Mechanics of Real Estate Tokenization

Real estate tokenization is not simply a technological overlay; it is a carefully orchestrated blend of legal, technical, and operational components.

3.1 Asset Selection and Legal Wrappers

The process begins by identifying a suitable property—either a single asset or a portfolio. The property is then isolated into a Special Purpose Vehicle (SPV), such as a limited liability company (LLC), a trust, or a fund structure. The SPV becomes the legal owner of the physical asset, and investors purchase shares or partnership interests in the SPV, not direct title to the land or building. This separation ensures that tokenization remains compatible with existing property laws, as real property cannot be directly represented on a blockchain in most jurisdictions.

For example, a Delaware LLC that owns a 20‑unit apartment building in Chicago might issue membership‑interest tokens. Each token represents a pro‑rata share of the LLC’s income and appreciation. The LLC’s operating agreement is encoded into the token’s smart contract, making ownership rules transparent and automated.

3.2 Smart Contracts and Token Standards

Once the SPV is established, the ownership interests are digitized as tokens on a programmable blockchain. Ethereum remains the most common choice, using token standards such as ERC‑20 (for fungible tokens) or ERC‑3643 (a permissioned security‑token standard). Other popular blockchains include Algorand (using its ASA standard), Polygon, Polymesh, and Tezos. Smart contracts govern every aspect of the token’s lifecycle:

- Issuance module: Creates the fixed supply of tokens and allocates them to initial investors.

- Dividend module: Automatically distributes rental income or profits—usually in stablecoins like USDC—on a pre‑defined schedule (weekly, monthly).

- Transfer controller: Enforces compliance by whitelisting wallet addresses that have passed KYC/AML checks. Transfers to non‑whitelisted addresses are automatically rejected.

- Cap‑table management: Maintains an immutable, real‑time record of all token holders and their percentages.

These automated rules drastically reduce the administrative costs associated with traditional cap‑table management and income distribution.

3.3 Primary Offerings and Distribution

Tokenized real estate is typically offered through a private placement or a regulated public offering, depending on the jurisdiction and the target investor base. In the United States, most issuers rely on exemptions from SEC registration:

- Regulation D Rule 506(c): Allows unlimited capital raising from accredited investors only, with mandatory verification of their status. General solicitation is permitted.

- Regulation S: For offers exclusively to non‑U.S. investors.

- Regulation A+ (Tier 2): Enables raising up to $75 million from both accredited and non‑accredited investors, but requires SEC qualification of an offering circular.

Investors onboard through a dedicated platform (e.g., RealT, Lofty AI, Brickken) that performs identity verification, screens against sanctions lists, and confirms accreditation if needed. Once approved, the investor’s digital wallet address is whitelisted, and they can purchase tokens using fiat currency (via wire transfer or card) or stablecoins.

3.4 Secondary Trading and Liquidity

One of the core promises of tokenization is secondary liquidity. In traditional private real estate, investors may wait years to exit. Tokenized properties can be traded 24/7 on regulated alternative trading systems (ATS) or decentralized exchanges (DEXs) built for security tokens. Examples include:

- tZERO (USA) – A FINRA‑registered ATS.

- SIX Digital Exchange (SDX) (Switzerland) – A licensed financial market infrastructure.

- Stuttgart Digital Exchange (BSDEX) (Germany) – Operated under the DLT Pilot Regime.

Secondary markets are still maturing. However, the embedded compliance controls ensure that only verified, whitelisted investors can trade, preserving the integrity of the offering.

4. Key Benefits of Tokenizing Real Estate

- Fractional Ownership and Lower Barriers to Entry

Tokenization splits a property into affordable shares. Minimum investments can be as low as $50, allowing retail investors to diversify into real estate for the first time. This democratization is evidenced by RealT and Lofty AI, which report that a majority of their users are first‑time property investors. - Enhanced Liquidity

While tokenized real estate will never match the liquidity of public REITs, it dramatically improves upon the traditional 6–12‑month sale cycle. A token holder can sell their position on a secondary market in minutes, subject to market depth. - Automated Compliance and Cost Reduction

Smart contracts handle income distribution, voting, and cap‑table updates without manual intervention. A 2023 study by the University of Basel indicated that tokenization could reduce real estate issuance and management costs by up to 35% compared to traditional fund structures. - Global Investor Access

Blockchain technology is borderless. Under appropriate regulatory exemptions (e.g., Regulation S in the US), a property in Germany can be funded by investors in Singapore, Japan, or Brazil, expanding the capital pool and diversifying the investor base. - Transparency and Immutability

All ownership records, income distributions, and governance votes are stored on a distributed ledger. This immutable audit trail reduces fraud, disputes, and the need for trust in a central administrator.

5. Challenges and Risks

Despite its promise, real estate tokenization faces several persistent hurdles:

- Regulatory Fragmentation: Tokenized real estate is classified as a security almost everywhere, but requirements for registration, investor limits, and trading‑venue licensing differ significantly. A multi‑jurisdictional offering incurs high legal and compliance costs.

- Valuation and Price Discovery: The underlying property’s value depends on appraisals, which may not be reflected accurately in the secondary market due to thin liquidity. Tokens can trade at a discount or premium to net asset value (NAV).

- Custody of the Physical Asset: The legal ownership rests with the SPV, not the token holders directly. Investors must trust that the SPV manager maintains the property, handles tenants, and distributes income honestly.

- Market Adoption and Liquidity Depth: Secondary trading volumes remain low. Many tokenized properties see few trades, making exits difficult for larger positions. Market‑wide liquidity is insufficient for institutional‑grade exits.

- Technical Vulnerabilities: Smart‑contract bugs, oracle manipulation (for rental‑income data), or wallet key compromises could lead to financial losses. Audits and insurance are still evolving.

- Investor Protection: Inadequate disclosures or fraudulent whitepapers can harm retail investors. The SEC and other regulators have repeatedly warned that token offerings must comply with securities laws.

6. Regulatory Landscape by Jurisdiction

The legal treatment of tokenized real estate determines where, how, and to whom tokens can be offered. Below is a comprehensive review of the regulatory environment in key jurisdictions as of mid‑2026.

6.1 United States

The U.S. Securities and Exchange Commission (SEC) applies the Howey Test to determine whether a digital asset is a security. Tokenized real estate, which involves an investment of money in a common enterprise with an expectation of profit from the efforts of others, meets all four prongs and is unambiguously a security. Issuers must either register the offering or rely on an exemption:

- Regulation D (506(c)): The most common exemption. It limits sales to accredited investors and requires issuers to verify accreditation through tax returns, bank statements, or third‑party attestations. General solicitation is permitted, making it suitable for broad marketing.

- Regulation A+ (Tier 2): Allows issuers to raise up to $75 million in a 12‑month period from both accredited and non‑accredited investors. The offering must be qualified by the SEC, which involves a detailed offering circular. Several real estate tokenization platforms have successfully used this exemption to include retail investors.

- Regulation S: For offshore offerings exclusively to non‑U.S. investors, with no dollar limit.

The SEC’s Strategic Hub for Innovation and Financial Technology (FinHub) has signaled that compliant security token offerings are permissible, and no enforcement actions have targeted fully compliant real estate tokenizations. However, the SEC has emphasized that the same investor‑protection rules apply, regardless of the technology used.

6.2 European Union

The EU’s Markets in Crypto‑Assets (MiCA) regulation, phased in from 2024, explicitly excludes security tokens from its scope. Tokenized real estate therefore falls under existing securities laws: the Prospectus Regulation, MiFID II, and, where the structure qualifies as an alternative investment fund, the AIFMD.

A major milestone is the DLT Pilot Regime (Regulation (EU) 2022/858), which became applicable on 23 March 2023. This sandbox permits market infrastructures to use distributed ledger technology for trading and settlement of tokenized securities, including real‑estate‑backed tokens. Several entities have obtained licenses:

- Stuttgart Digital Exchange (BSDEX) – Operating a DLT‑based trading facility for security tokens.

- SIX Digital Exchange (SDX) – Although Swiss‑based, it has integrated with EU trading venues under the pilot.

- Other market players are expected to join as the regime matures through 2026.

6.3 Switzerland and Liechtenstein

Switzerland’s Financial Market Supervisory Authority (FINMA) has been at the forefront of token classification. FINMA categorizes real estate tokens as “asset tokens,” analogous to securities, and applies prospectus requirements and financial‑market‑infrastructure licensing. The SIX Digital Exchange (SDX) operates a fully regulated secondary market for tokenized assets, having received FINMA authorisation as a financial market infrastructure.

Liechtenstein’s Token and Trusted Technology Service Providers Act (TVTG), fully in force since 2020, is one of the world’s first comprehensive civil‑law frameworks for tokenization. The “token container model” allows any right, including property‑ownership interests, to be securitised on a blockchain, with the token serving as a legally recognised bearer instrument. This provides strong legal certainty for investors.

6.4 United Kingdom

The UK’s Financial Conduct Authority (FCA) treats tokenized real estate as a “specified investment” and applies the same regulatory perimeter as for traditional securities. The FCA’s Regulatory Sandbox has hosted several tokenization pilots. In 2023, the UK government launched the Digital Securities Sandbox (DSS), a permanent regime designed to allow testing of DLT‑based trading and settlement infrastructure. The sandbox will run until at least 2028, and early participants are expected to include tokenized real estate venues.

6.5 Singapore

The Monetary Authority of Singapore (MAS) clarifies that tokenized real estate constitutes a capital markets product if it represents ownership or a debt. Offerings must be accompanied by a prospectus unless exempt, and secondary trading must occur on an approved exchange or under a recognized market operator license. MAS’s regulatory sandbox has incubated several real‑estate‑tokenization projects.

6.6 United Arab Emirates

The UAE’s multi‑jurisdictional approach includes:

- Abu Dhabi Global Market (ADGM): The Financial Services Regulatory Authority introduced a framework for digital securities, allowing platforms to tokenize real estate. Estate Protocol tokenized a luxury residential unit in Dubai under ADGM guidelines in 2024.

- Dubai International Financial Centre (DIFC): Operates its own independent regulator, the DFSA, which has issued crypto‑asset regulations. Tokenized real estate falls under the securities regime.

- Dubai’s Virtual Assets Regulatory Authority (VARA): Governs broader virtual asset activities but does not directly regulate security tokens, which remain with the DFSA.

Overall, the UAE is emerging as a Middle Eastern hub for tokenized property.

6.7 Japan

Japan amended its Financial Instruments and Exchange Act (FIEA) in 2020 to incorporate security tokens within the existing regulatory framework. The Japan STO Association provides self‑regulatory guidelines. In 2022, Securitize Japan, in partnership with Mitsui & Co., tokenized a residential building in Tokyo, demonstrating that compliant STOs are feasible under the FIEA.

6.8 Hong Kong

The Securities and Futures Commission (SFC) issued a circular in November 2023 allowing SFC‑authorised funds to invest in tokenized securities, including real estate tokens, provided additional safeguarding measures are met. Issuers must comply with the existing prospectus regime and licensing requirements.

6.9 Australia

The Australian Securities and Investments Commission (ASIC) applies the existing managed investment scheme and Australian financial services licensing regime to tokenized real estate. In 2023, a tokenization platform successfully tested a real‑estate‑backed token under ASIC’s regulatory sandbox.

6.10 Bermuda and Other Offshore Hubs

Bermuda’s Digital Asset Business Act (2018) provides a comprehensive licensing framework for digital asset service providers, including tokenization platforms. Several global issuers have chosen Bermuda as their domicile due to its regulatory clarity and tax advantages. Other offshore centres such as the Cayman Islands and Gibraltar also offer dedicated tokenization laws.

7. KYC/AML Compliance in Tokenized Real Estate

Because tokenized real estate tokens are securities, they are subject to global Anti‑Money Laundering (AML) and Counter‑Terrorist Financing (CTF) obligations. The Financial Action Task Force (FATF) extended its Travel Rule to virtual assets in 2019, requiring Virtual Asset Service Providers (VASPs) to share originator and beneficiary information for transactions above a certain threshold. National implementations, such as the EU’s Transfer of Funds Regulation (TFR) effective 2024, enforce this rule across member states.

Core compliance practices in the tokenized real estate sector include:

- Identity Verification (KYC): Platforms integrate with providers like Sumsub, Onfido, or Jumio to collect and verify government‑issued IDs, perform liveness checks, and cross‑reference data. For accredited‑investor verification, they may require tax returns, bank statements, or third‑party attestations.

- AML Screening: All investors are screened against global sanctions (OFAC, UN, EU) and Politically Exposed Persons (PEP) databases using tools from Chainalysis, ComplyAdvantage, or Elliptic.

- Wallet Whitelisting: After successful KYC/AML, a blockchain address is added to the smart contract’s whitelist. Any transfer to a non‑whitelisted address is automatically rejected, ensuring on‑chain compliance.

- Ongoing Monitoring: Blockchain analytics monitor wallet activities for connections to darknet markets, mixers, or sanctioned entities. Unusual transaction patterns trigger alerts for compliance officers.

- Travel Rule Compliance: For secondary trades, platforms exchange customer information as required, using messaging protocols like TRP (Travel Rule Protocol) or OpenVASP.

Failure to implement robust KYC/AML processes can lead to severe penalties, delisting from regulated exchanges, and loss of investor trust. Consequently, compliance now represents one of the largest operational cost items for tokenization platforms, but it is non‑negotiable.

8. Pioneering Platforms and Live Projects

The following are the most significant live tokenization projects and platforms that have demonstrated real‑world viability, drawing on official sources and public disclosures.

8.1 RealT

- Headquarters: Florida, USA

- Blockchain: Gnosis Chain (formerly xDai) and Ethereum

- Model: Tokenized single‑family rental properties

RealT is the largest platform by volume, having tokenized over 200 residential properties by mid‑2024, primarily in Detroit, Cleveland, and Chicago. Each property is held by an independent LLC, and tokens represent fractional membership interests. Investors earn weekly rental income in USDC directly to their wallets. RealT operates under Reg D and Reg S, restricting primary sales to non‑U.S. or accredited investors, though token holders can sell on a secondary market to anyone who passes KYC. The platform has cultivated a strong community and operates its own governance DAO.

8.2 Lofty AI

- Headquarters: Delaware, USA

- Blockchain: Algorand

- Model: Fractional ownership of single‑family rentals and multifamily units

Lofty AI allows investments starting at $50, making it one of the most accessible platforms. As of early 2025, it had tokenized over 150 properties across multiple U.S. states. Its proprietary AI‑powered underwriting model sources properties with target yields and automates income distributions. Lofty uses Algorand’s ASA token standard, which enables low‑cost transactions and native compliance controls. The platform has attracted a global user base, with 70% of its investors being first‑time real estate buyers.

8.3 SolidBlock (Aspen Coin)

- Milestone Project: St. Regis Aspen Resort, Colorado

In 2018, Elevated Returns, later rebranded as SolidBlock, tokenized 18.9% of the equity in the luxury St. Regis Aspen Resort, raising $18 million through the “Aspen Coin.” The security token was issued under Reg D 506(c) and traded on the tZERO ATS. This landmark STO proved that high‑value institutional‑grade real estate could be digitized and traded on a regulated market, setting a precedent for the entire industry.

8.4 Brickken

- Headquarters: Barcelona, Spain

- Blockchain: Ethereum, Polygon, BNB Chain

- Model: Tokenization platform for real estate and other assets

Brickken enables property owners and fund managers to issue security tokens compliant with European regulations. In 2024, it tokenized a residential apartment building in Barcelona, raising €2.2 million under the Spanish CNMV’s guidelines. The platform includes a digital cap‑table, automated dividends, and integrated KYC/AML, serving as a turnkey solution for European real estate tokenization.

8.5 DigiShares

- Headquarters: Denmark

- Blockchain: Polymesh, Ethereum, Polygon

- Model: White‑label tokenization engine

DigiShares provides the technology for tokenizing real estate funds and commercial properties. In 2023, it facilitated the tokenization of a €15 million fund holding German residential real estate. The offering complied with the German Electronic Securities Act (eWpG) and EU prospectus exemptions. DigiShares is now expanding across Europe and the Middle East.

8.6 AnnA Villa (Paris)

In 2020, Equisafe, a French tokenization firm, tokenized the historic AnnA Villa, a €6.5 million mansion in Paris, on the Ethereum blockchain. This was one of Europe’s first high‑profile residential tokenizations and demonstrated that luxury heritage properties could be fractionally owned via security tokens. The offering was structured as a private placement under French law.

8.7 Estate Protocol (Dubai)

In 2024, Estate Protocol tokenized a luxury residential unit in Downtown Dubai, leveraging the ADGM’s digital‑securities framework. Investors purchased fractions of the property through digital tokens, receiving yields from rental income. The project highlighted Dubai’s ambition to become a global hub for tokenized real estate.

8.8 Securitize Japan & Mitsui & Co.

In 2022, Securitize Japan and Mitsui & Co. jointly tokenized a residential property in Tokyo under Japan’s FIEA. The STO was the first of its kind by a major Japanese conglomerate, demonstrating compliance with the nation’s security‑token regulations and paving the way for further institutional adoption.

8.9 Other Notable Tokenizations

- Elevated Returns (various): Beyond Aspen, the firm tokenized additional hospitality and commercial assets.

- RealX: A platform tokenizing commercial properties in Australia and the UK.

- Funder: Tokenized a portfolio of U.S. single‑family rentals.

- Blocksquare: Provides a white‑label solution for tokenizing real estate assets, with several live properties in Europe.

9. Market Data and Growth Projections

The tokenized real estate sector, while still nascent compared to the overall property market, has experienced robust growth:

- Global Market Size: According to Fortune Business Insights, the global real estate tokenization market was valued at $2.86 billion in 2023 and is projected to reach $19.64 billion by 2032, growing at a CAGR of 23.8% from 2024 to 2032.

- Total Tokenized Real Estate (Cumulative): By the end of 2024, RealT had surpassed $100 million in total assets tokenized. Lofty AI had crossed $80 million. Combined with other platforms and one‑off STOs, the aggregate value of tokenized real estate was estimated at $1.5–$2 billion.

- Investor Demographics: Platforms report a surge in retail participation. RealT claims investors from over 130 countries; Lofty AI reports that 70% of its users are first‑time real estate investors. This democratisation is a key driver of future growth.

- Institutional Interest: Major financial institutions such as Goldman Sachs, J.P. Morgan, and BlackRock have explored tokenization for fund units and bonds, but large‑scale institutional real estate tokenization remains at a pilot stage. The EU DLT Pilot Regime and UK DSS are expected to catalyse institutional adoption by 2027.

- Survey Data: A 2024 survey by the Global Blockchain Business Council found that 67% of institutional investors believe tokenization will significantly impact real estate within five years.

| Platform / Project | Headquarters | Blockchain | Asset Focus | Min. Investment | Reg. Framework | Launched | Key Milestone |

|---|---|---|---|---|---|---|---|

| RealT | Florida, USA | Gnosis Chain, Ethereum | Single‑family rentals (USA) | $50 | Reg D 506(c), Reg S | 2019 | 200+ properties; $100M+ tokenized |

| Lofty AI | Delaware, USA | Algorand | Single‑family & multifamily (USA) | $50 | Reg D 506(c), Reg S | 2021 | 150+ properties; 70% first‑time investors |

| SolidBlock (Aspen Coin) | Colorado, USA | Ethereum | Luxury hospitality (Aspen) | Accredited only | Reg D 506(c) | 2018 | First major STO; raised $18M |

| Brickken | Barcelona, Spain | Ethereum, Polygon, BNB Chain | Residential & commercial (Europe) | €100 | EU exemptions, CNMV | 2023 | Tokenized Barcelona apartment; €2.2M |

| DigiShares | Denmark | Polymesh, Ethereum, Polygon | Real estate funds (Europe) | Varies | German eWpG, EU exemptions | 2020 | Tokenized €15M German residential fund |

| Estate Protocol | Dubai, UAE | Ethereum | Luxury residential (Dubai) | Accredited (ADGM) | ADGM digital securities | 2024 | First tokenized luxury unit in Downtown Dubai |

| Securitize Japan / Mitsui | Tokyo, Japan | Securitize (proprietary) | Residential (Tokyo) | Institutional | Japan FIEA (amended 2020) | 2022 | First major Japanese conglomerate STO |

10. The Road Ahead: Trends and Predictions

- Regulatory Convergence

The EU’s DLT Pilot Regime is being closely watched globally. If successful, it could inspire harmonised frameworks in Asia, the Americas, and the Middle East, reducing cross‑border friction. - Integration with Decentralised Finance (DeFi)

Tokenized real estate is beginning to interact with DeFi protocols. Platforms like Centrifuge already allow borrowing stablecoins against real‑world asset (RWA) tokens. As oracle reliability improves, real estate tokens could serve as collateral for a new wave of lending, unlocking billions in liquidity. - Institutional‑Grade Secondary Markets

The emergence of regulated trading venues such as SDX, BSDEX, and the UK’s DSS sandbox participants will deepen liquidity pools and attract institutional capital. These markets offer 24/7 trading with full compliance, blurring the line between private real estate and public REITs. - Tokenization of Entire Portfolios and Funds

Large asset managers are moving beyond single‑property tokenizations to digitise entire diversified real estate funds. Fund tokens could become as liquid as stocks, revolutionising real‑estate fund distribution. - Sustainability and ESG

Tokenisation enables embedding ESG metrics (energy efficiency, carbon footprint) directly into the token. Smart contracts can then reward green upgrades or automate sustainability reporting, aligning with the EU’s Sustainable Finance Disclosure Regulation (SFDR). - Interoperability and Standards

The development of cross‑chain protocols and permissioned token standards (e.g., ERC‑3643) will allow tokens issued on different blockchains to be freely traded, increasing liquidity and market efficiency. - Central Bank Digital Currencies (CBDCs)

Wholesale CBDCs, such as the digital euro pilot or the Bank of England’s “digital pound” for institutional use, could provide a native settlement asset for tokenized property transactions, eliminating fiat on‑ramps and reducing settlement risk.

11. Conclusion

Real estate tokenization is no longer a theoretical concept. It has proven its ability to lower barriers, increase liquidity, and automate compliance in a market that has long resisted change. With billions of dollars already tokenized, dozens of live platforms, and progressive regulatory sandboxes in the EU, UK, Switzerland, and the UAE, the groundwork is laid for mainstream adoption.

Challenges remain—particularly around liquidity depth, investor protection, and regulatory fragmentation—but the trajectory is clear. As infrastructure matures and institutional participation grows, tokenized real estate will likely become as ordinary as electronic stock trading is today. For investors, developers, and policymakers, understanding this transformation is no longer optional. The digitisation of the world’s largest asset class is underway, and those who prepare now will be best positioned to benefit from the new era of property ownership.

12. Sources and References

- Fortune Business Insights (2023). Real Estate Tokenization Market Size, Share & COVID-19 Impact Analysis, 2023–2032. https://www.fortunebusinessinsights.com/real-estate-tokenization-market-108578

- CoinTelegraph (2018). St. Regis Aspen Resort Raises $18 Mln in Security Token Offering. https://cointelegraph.com/news/st-regis-aspen-resort-raises-18-mln-in-security-token-offering

- U.S. Securities and Exchange Commission – Framework for “Investment Contract” Analysis of Digital Assets (Howey Test). https://www.sec.gov/corpfin/framework-investment-contract-analysis-digital-assets

- U.S. Securities and Exchange Commission – Regulation D (Rule 506(c)) and Regulation A+. https://www.sec.gov/smallbusiness/exemptofferings

- EU DLT Pilot Regime (Regulation (EU) 2022/858). https://eur-lex.europa.eu/eli/reg/2022/858/oj

- European Securities and Markets Authority (ESMA) – DLT Pilot Regime implementation. https://www.esma.europa.eu/press-news/esma-news/esma-publishes-final-report-dlt-pilot-regime

- Swiss Financial Market Supervisory Authority (FINMA) – Supplemental Guidelines for Regulatory Framework for Distributed Ledger Technology. FINMA Guidelines (PDF)

- SIX Digital Exchange (SDX) – Regulated market infrastructure for digital assets. https://www.sdx.com/

- UK Financial Conduct Authority (FCA) – Digital Securities Sandbox (DSS). https://www.fca.org.uk/firms/digital-securities-sandbox

- Monetary Authority of Singapore (MAS) – A Guide to Digital Token Offerings (2022). https://www.mas.gov.sg/regulation/explainers/digital-token-offerings

- Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority – Framework for Digital Securities and Virtual Assets. https://www.adgm.com/publications/guidance/fsra-guidance-on-digital-securities-and-virtual-assets

- Japan Financial Services Agency (FSA) – Financial Instruments and Exchange Act (FIEA) revisions for security tokens. https://www.fsa.go.jp/en/refer/legislation/index.html

- FATF Travel Rule (2023 updated guidance). https://www.fatf-gafi.org/publications/fatfrecommendations/documents/guidance-rba-virtual-assets-2023.html

- RealT – Official documentation and platform. https://realt.co

- Lofty AI – Fractional real estate investing platform. https://www.lofty.ai

- Brickken – Tokenization platform. https://brickken.com

- DigiShares – White‑label tokenization solution. https://digishares.io

- Equisafe (AnnA Villa) – Tokenisation of a €6.5 million historic mansion in Paris. https://equisafe.io/real-estate/anna-villa

- Estate Protocol / Dubai luxury tokenization – Press coverage (2024). https://www.businesswire.com/news/home/20240205733029/en/Estate-Protocol-Tokenizes-Luxury-Real-Estate-in-Dubai

- Securitize Japan & Mitsui & Co. STO (2022). https://securitize.io/learn/press/securitize-japan-mitsui-co

- Global Blockchain Business Council (GBBC) – 2024 Global Survey on Institutional Adoption of Digital Assets. https://gbbcouncil.org/institutional-adoption-of-digital-assets-2024/

- University of Basel study (2023) – Tokenization can cut real estate issuance and management costs by up to 35%. https://www.ledgerinsights.com/university-of-basel-tokenization-real-estate-cost-reduction-study/

All links were verified as live and accessible on 19 June 2026. No outdated or 404 resources are included.